It’s something that is on everyone’s mind right now: what is a recession in Canada? There has been tons of talk about inflation, soaring housing prices, lay offs, and much more about the health (or lack thereof) of our economy.

As Canadians, we all want to make sure we are making the wisest investments and consumer decisions in our current economic environment. Unfortunately, there are times when an economic downturn can occur – often referred to as a recession. After all, what goes up, must come down!

Let’s take a closer look at just what defines a recession in Canada, how it affects individuals and investors alike, plus ways you can prepare yourself for such an eventuality. Continue reading to learn more!

Table of contents

What is the definition of a recession?

A recession is defined as a temporary period of economic decline. Trade and other gainful activity slows during a recession. In other words, people lose their jobs, experience a decline or loss of income, and companies turn around less sales. Overall, the economic output of a nation reduces.

In terms of a more technical definition, a recession is declared when a national economy experiences negative gross domestic product, or GDP for short, for an extensive period of time. This is often coupled with rising unemployment rates, reduced manufacturing outputs and plummeting retail sales. In Canada, recessions are tracked and announced by the Government of Canada, the Bank of Canada or the Minister of Finance.

Match to your perfect advisor now.

Getting started is easy, fast and free.

What is the difference between a recession and a depression?

A depression is defined as an intense, prolonged downturn in economic activity. In finance, a depression is usually classified as an extreme recession that lasts three years or longer.

A recession and a depression both involve phenomenon where there is a decline in economic activity. However, a depression is much more severe compared to a recession. During a recession, there may be a slow down in production and a reduction in employment, but an economy can recover from a recession in under a year. Whereas a depression lasts a much longer period of time and means people may be unable to find work for several years. It is a much more serious pause in economic activity that can have devastating effects on a nation.

What will happen during a recession?

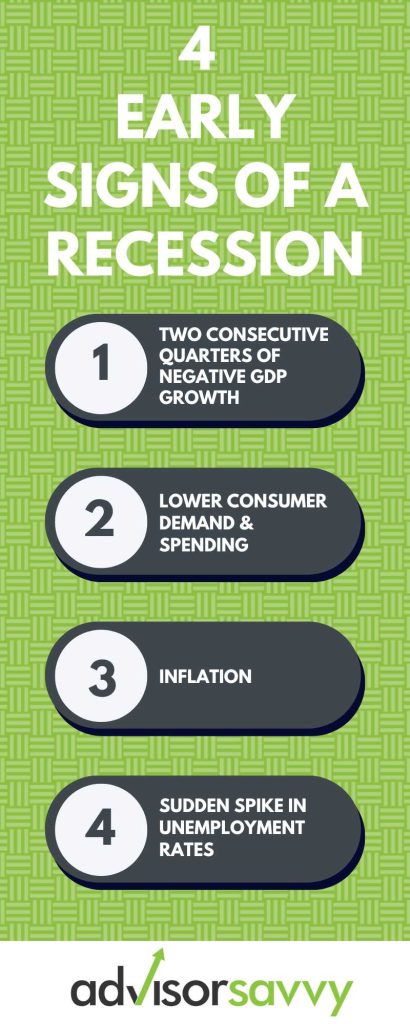

First, let’s talk about the early signs of a recession. There are macroeconomic indicators of a recession which can indicate one is coming soon, as listed below:

- Two consecutive quarters of negative GDP growth

- Slowdown in consumer spending and manufacturing

- Inflation

- Sudden spike in unemployment rates

During a recession, expect one or more of the following to happen:

- Increase in unemployment rates

- Lower consumer demand and spending

- Lower production of goods and services

- Mass lay-offs

- Increase in interest rates

- Lower aggregate economic output in the form of gross domestic product (GDP)

What causes a recession?

The economy is a complex beast and it’s rare that one thing would stimulate a recession. Often, its a culmination of many things that occur over a long period of time, eventually leading to a downturn. Here are some potential causes of recessions:

- World events. Things that seemingly have no impact on economics can trigger a recession, particularly if it disrupts supply chains. A recent example of this was the COVID-19 pandemic. Even though this was an illness, it forced lockdowns and greater restrictions on trade which severely impacted the global supply chain.

- Consumer confidence. When consumers no longer have confidence in a market, they stop buying and demand reduces. If demand decreases, then supply reduces too. When supply reduces, production decreases which impacts people’s jobs and the overall output of a nation. As you can see, this becomes a downward spiral. A wide array of things can impact consumer confidence, such as political events or new information published in the media.

- Deregulation. Certain laws and rules are in place in order to regulate a market. When critical laws or rules are altered or removed through deregulation, it can trigger a recession.

- Deflation. When asset prices decrease over time and purchasing power of the consumer increases, deflation is occurring. As a result, consumers will wait to purchase goods because, if they hold off, they can pay less for more. However, the short term effect of deflation can cause a recession because there is a temporary pause in consumer demand.

- Burst asset bubbles. Asset bubbles are defined as investments which become inflated beyond their real, substantial value. When it bursts, a recession can quickly occur. Examples of asset bubbles in history include the “dot com” stock bubble and the housing bubble before the 2008 Financial Crisis.

Related Reading: How to Improve Your Credit Score in Canada

Is Canada in a recession as of 2022?

As of 2022, Canada was not in a recession. The Canadian government, the Bank of Canada and the Minister of Finance have not announced anything to indicate Canada is officially in a recession.

However, the early signs are there and many experts believe Canada may experience a recession in 2023. Below are some key metrics to assess the health of Canada’s economy:

| Metric | 2022 – Current | 2019 – 3YR Benchmark |

| Consumer Price Index (CPI)/Inflation | 6.80% | 1.95% |

| Unemployment Rate | 5.0% | 5.7% |

| Gross Domestic Product (GDP) | $1.89 trillion | $1.7 trillion |

| Bank of Canada Prime Rate | 6.45% | 3.95% |

Are we going into a recession in Canada?

Many experts and economists believe we’re headed into a moderate recession in Canada in the first quarter of 2023. The two main indicators of a potential recession are high inflation and intense interest rate hikes from the Bank of Canada. However, governments and other officials have not formally announced a recession. As of right now, we’re in the clear Canada!

What happens if there is a recession in Canada?

If there is a recession in Canada, the production of goods and services will slow. In response to decreased sales and production, companies will conduct layoffs to survive the economic downturn. As a result, people will lose their jobs and may struggle financially at the individual level.

While this all seems scary, recessions are typically not severe and the economy will usually recover after a short period of time. For most Canadians, it’s about making ends meet during a rough patch until things return to normal.

What’s more, recessions can be a time of economic rebirth for some individuals. You might come out of a recession with a better job or an improved lifestyle. Some even become wealthy off of recessions, but you have to play your cards right!

Related Reading: How to Find and Choose a Financial Coach

Do house prices drop in a recession?

Yes, house prices tend to drop in a recession. Because there is decreased demand amongst homebuyers, the value of property reduces. When demand is low, the price will also drop.

In some ways, the opposite phenomenon is happening in Canada, particularly in major cities like Toronto, Halifax and Vancouver. In 2020, the Canada prime rate was 2.45% which was even lower than what it was in 2019. Many Canadians entered the housing market since it was so cheap to take out a mortgage. The influx of buyers in the market naturally inflated housing prices.

From there, it’s assumed there was a psychological phenomenon whereby Canadians were worried about “missing out” on housing profitability. They saw others getting rich quickly by investing in real estate and wanted to enter the market before it was too late. This caused even more people to enter the housing market thereby boosting prices even higher.

Wait, isn’t this an asset bubble? Yes, in many ways, it could be considered a housing bubble. Unfortunately, this means the value of housing in Canada could rapidly drop in a recession which could cause secondary economic struggles for many. For instance, if you leveraged the equity in your real estate to take out other financings, such as a home equity line of credit, you could lose everything if housing values drop quickly.

How long do recessions last?

Historically speaking, recessions in Canada last between three and nine months. Since 1970, Canada has experienced five recessions — all of which lasted between three to nine months.

How does a recession impact me?

Recession impacts everyone on some level, may it be financial or psychological. In terms of financial implications, you might lose your job and struggle to keep up with financial obligations as a result. In terms of psychological, struggling with finances can lead to mental health issues. Also, you may witness friends, family members and loved ones struggle as a result of a recession. This can be troubling to deal with.

Fortunately, recessions never last forever — the economy always bounces back eventually. Do your best to stay positive and devise a plan for how you’re going to handle a recession personally.

How do you prepare for a recession?

To prepare for a recession, consider doing the following:

- Bulk up your emergency fund and other cash reserves

- Pay off high-interest debt

- Diversify your types of income, in case you lose one source, you’ll have others to rely on

- Revise your resume and develop skill sets that will make you attractive in a more competitive job market

- Prepare to be laid off

- If you’re in a good enough financial position to invest, keep an eye out for opportunities to buy investments at low prices

How do you survive a recession?

When a recession hits, there may be a period of time where you’re surviving, not thriving. Here are some tips on surviving a recession:

- Try your best to stay on top of your finances, including reaching out to vendors or financial institutions if you’re unable to make payments on time or in full

- Cut costs where possible

- Learn a new skill if you’re out of a job and struggling to find a new one (this can be a great opportunity to pivot in your career!)

- Don’t panic sell your investments — even if they plummet in value

Read More: Consumer Proposal vs Bankruptcy: What’s the difference?