An emergency fund is an important part of your financial health and security. It can help you cover unexpected expenses, like a car repairs or medical bills. Plus, an emergency fund can protect you from falling into a cycle of debt. Just knowing you have funds available in the event of an emergency can provide greater peace of mind too. But what is an emergency fund in Canada exactly? And how much should you save? Here’s what you need to know about an emergency fund in Canada and why they are important.

Table of contents

What is an emergency fund?

An emergency fund is a valuable resource that can help you stay financially prepared for unexpected costs and stressful situations. This type of fund consists of money you set aside for use in the event of a sudden need, such as an injury or suddenly being laid off. Normally, an emergency fund is a lump sum of cash that’s set aside and readily available for use at any point in time.

The main benefit of having an emergency fund in Canada is it allows you to smooth out fluctuations in your budget and avoid falling into debt when dealing with difficult circumstances. Additionally, having this type of savings account can give you peace of mind knowing you are able to manage unexpected expenses without derailing your plans or finances.

Why is an emergency fund important?

An emergency fund is an important financial resource for anyone to have. It provides a safety net in case of unexpected expenses, such as costly medical bills or car repairs. By having this extra cushion of funds, you can avoid having to rely on debts when you suddenly need money.

Furthermore, an emergency fund can help you maintain a healthy cash flow, even during difficult periods when your income might be temporarily interrupted. Alternatively, it can aid cash flow when you have an unexpected expense.

Overall, an emergency fund is essential for protecting yourself against financial hardship and maintaining greater stability in your personal and professional life.

What should the emergency fund cover?

An emergency fund can cover an array of costs. Below are possible events or circumstances where you may need to tap into an emergency fund:

- Urgent car repairs

- Medical costs not covered by OHIP or insurance

- Unexpected vet costs for your pet (if you don’t have pet insurance)

- Living expenses when you suddenly lose your job

- Urgent home renovations or repairs (such as a leaky roof or flooded basement)

- Unexpected travel costs (such as attending a funeral or seeing a sick loved one)

Who needs an emergency fund in Canada?

An emergency fund is an essential tool for anyone who wants to save and protect themselves financially. In other words, every Canadian should have an emergency fund to maintain adequate financial health. However, certain Canadians need an emergency fund more than others, including:

- Households with children

- Individuals and households with high debt and financial leverage

- Individuals and households with one income source

Related Reading: What is Financial Planning?

How to build an emergency fund in Canada

While the exact amount that should go into your emergency fund may vary depending on your personal situation, there are several key principles to keep in mind when setting up and managing this important financial tool.

For starters, be sure to build your fund slowly, but steadily over time. This will help you avoid dipping into it for other expenses or taking on debt. Put your emergency savings as a top priority by budgeting a fixed percentage of your income to it each month. Once you achieve your emergency fund goal amount, you can continue to set aside money in the form of long term savings for further financial stability.

How much money should be in an emergency fund?

There is no set amount that constitutes an “appropriate” level of savings for an emergency fund. Different people will have different needs and expenses. What might be enough for one individual may not be sufficient for another.

That being said, most experts recommend having at least 3 to 6 months of living expenses saved up in the event of sudden financial hardship or job loss. This can help to provide stability and security during difficult times, giving you greater peace of mind as you work through whatever challenges you might encounter.

Some people may argue that a small amount, such as $1,000, is sufficient and will enable you to deal with the most basic financial emergencies, such as car repairs or unexpected medical bills. However, others might argue that a larger amount, such as $10,000 or more, would be more beneficial for ensuring your long-term financial security. Ultimately, the amount of money that you should have in your emergency fund will depend on many factors, including your income level, risk tolerance, lifestyle and living expenses.

However, one thing most experts would agree on is that having some funds set aside for unexpected expenses is essential for managing financial uncertainty and helping you avoid potential debt or hardship in the future.

Related Reading: Canada Debt: How much is too much?

How many months should an emergency fund cover?

Some prefer to look at an emergency fund in Canada as the dollar amount, while others prefer to quantify it as the number of months of living expenses it will cover. If you choose the latter metric, a good benchmark is 3 to 6 months of living expenses. This is particularly ideal in the event of job loss because it can take around 3 to 6 months to find a new job.

Tips to set up an emergency fund

Ready to start building your emergency fund? Here’s some tips and tricks to get you started on the right foot.

Open a savings account

Opening a savings account is an essential step toward financially securing your future. Because savings accounts typically carry low levels of risk and reliably earn interest over time, they are a great way to start building up an emergency fund that you can access in the years to come.

In addition, having a separate account for your emergency fund can help you maintain separation in your finances. This can help you avoid the temptation of using your emergency fund for other expenditures.

Helpful Tool: Savings Calculator

Start by saving a realistic amount

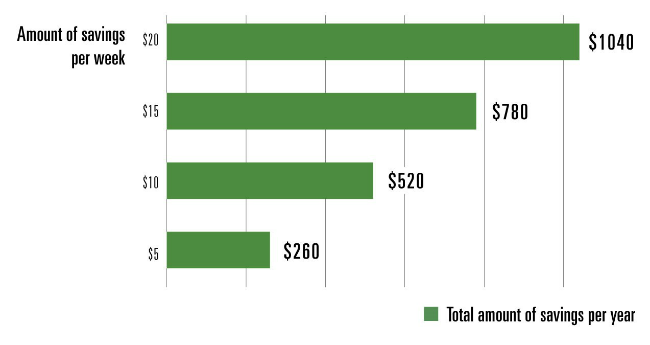

Saving can be a challenging habit to form if you aren’t already in the practice. However, start by saving a realistic amount based on your income and expenses. Even if it’s a small amount, it can still go a long way. In fact, this chart shows how a little bit of money can build a basic emergency fund in Canada in just one year:

Make it a habit

Making regular savings a part of your everyday routine can be one of the most effective ways to build long-term financial stability. Whether you’re saving for a long-term goal like retirement or simply setting aside money for emergencies, staying consistent with your savings habits is key. It’s hard to form a new habit, but just remember your financial goals whenever you feel like caving. Even beyond your emergency fund, you should continue saving towards other goals. This is not a habit you’ll regret forming!

Automate your savings

Using automatic savings can help you stick to your goals without having to think about it too deeply. Select an amount, date, and frequency for saving money by setting up an automatic account transfer from your regular account to your savings account. You may set up your automatic transfer on the days you get paid. As soon as your pay cheque is credited to your account, the amount will be transferred.

Eliminate an expense and save the amount

Some costs can be cut, and these amounts might be added to your emergency fund. This won’t have any impact on your existing budget or the speed at which you build up your savings. Identify the gap between your demands and wants to determine the expenses you can save.

To minimize needless expenses, try one or more of the following:

- Bring your lunch to work instead of buying it

- Make your coffee at home instead of buying a $5 latte everyday

- Use public transportation rather than driving your automobile

- Remove one non-essential food choice from your grocery list

- Make use of discounts, cashback offers, and other deals to save money on everything you buy.

- Use utilities less in peak hours when the rates are more expensive

- Eliminate expenses from your budget that you’re not using

- Sell things around your home that you’re not using on platforms like Facebook or Kijiji

Increase your emergency fund

Deposit any additional money into your savings account whenever possible to help increase your emergency fund. For instance, if you receive a bonus at work or a hefty tax refund, consider putting it towards your emergency fund instead of spending it.

Related Reading: Budgeting Tips for Canadians

Be prepared for anything with an emergency fund in Canada

When it comes to financial health, having an emergency fund is one of the most important things to consider. An emergency fund allows you to be prepared for any situation that might arise, from the sudden loss of a job to the unexpected expense of a medical emergency.

By having a reserve of funds that you can access quickly and easily in times of need, your financial well-being will be secured and you will be equipped to deal with whatever life throws your way. Whether you are just starting out with savings or looking to bolster your current accounts, taking steps to build an emergency fund is a sign of good financial health and will help put you on the path to success. Don’t hesitate – start preparing for anything with an emergency fund today!

Read More: How to Invest $1,000, $10,000 or $100,000